Waymo’s driverless Chrysler Pacificas glide silently through Phoenix rush hour, no human at the wheel, racking up 250,000 paid rides every week.

That’s not a demo. It’s revenue—real money changing hands as autonomous driving hits commercial stride after decades of hype and crashes.

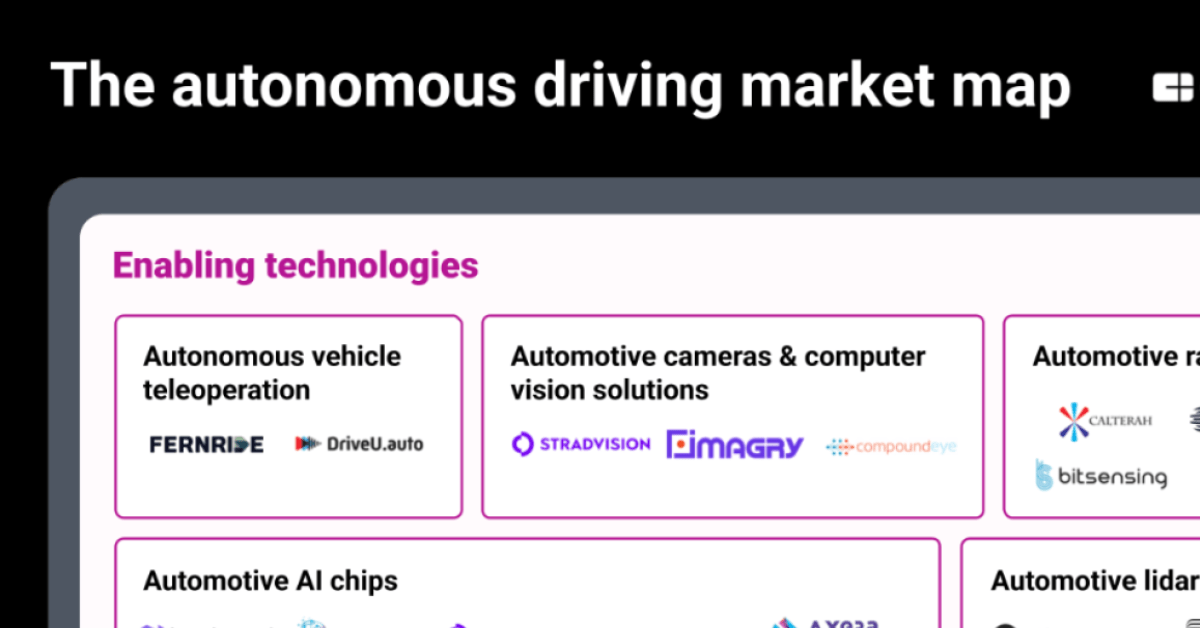

Zoom out. Using CB Insights data, we’ve mapped over 90 private companies and key subsidiaries across 14 categories, from gritty sensor makers to hulking industrial truck builders. This isn’t just a directory; it’s a battlefield where momentum clusters, and winners will dictate how we move.

“Waymo now operates over 2,000 robotaxis, completing 250,000+ weekly paid rides across multiple US cities. Baidu completed over 17M rides in China with its Apollo Go robotaxi, while Tesla launched its robotaxi service in June 2025.”

Those numbers? They’re the smoke signaling fire. But beneath the rides lie architectural shifts—enabling technologies like lidar arrays and simulation engines feeding into autonomous driving platforms, all converging on vehicle development for trucks, delivery bots, and yes, your next Uber.

Who’s Hoarding the Momentum in Enabling Tech?

Sensors first—lidar, radar, cameras. Companies like Luminar and Innoviz aren’t sexy names, but they’re the eyes of the beast. Picture this: a self-driving stack demands 360-degree perception at highway speeds, fusing data from spinning lasers that cost as much as a used Honda just years ago. Prices plummet—Luminar’s units now dip under $1,000—thanks to scale and chip advances.

Mapping tools? Here’s where it gets sneaky. Mobileye (Intel’s arm) and HERE Technologies build HD maps that update in real-time, slurping lidar scans from fleets to refine every pothole. It’s a flywheel: more miles driven, better maps, safer rides.

But simulation—ah, that’s the dark magic. Ansys, Applied Intuition. They craft virtual worlds where cars “drive” billions of edge-case miles overnight. Why? Real-world testing kills—literally, and legally. One glitch in sim saves a recall.

Short para: Winners here own the picks-and-shovels.

Why Platforms Are the New Oil Barons

Autonomous driving platforms stitch it all: foundation models trained on petabytes of drive data. NVIDIA’s Drive Orin? It’s the GPU heart pumping AI inferences at 254 TOPS. Cruise (GM), Zoox (Amazon)—they’re stacking these into full-stack software that ports across cars, trucks, drones.

Tesla’s edge? Its Full Self-Driving beta, hoovering 6 billion miles from owners’ cars. No lidar—just vision and neural nets. Bold. Risky. But if it scales, Elon skips the sensor tax.

Baidu’s Apollo Go? 17 million rides in Wuhan alone. China’s regulatory green light—faster than California’s DMV slog—lets them iterate brutally.

Here’s my take, absent from the original map: this mirrors the 1990s browser wars. Netscape built the best tools, but Microsoft bundled IE into Windows and crushed them. Platforms like Tesla or Waymo (Alphabet-backed) will bundle and commoditize enablers, concentrating value upstream. Don’t bet on sensor pureplays long-term.

Vehicles: From Robotaxis to Warehouse Beasts

Commercial fleets lead. Waymo One in SF, Austin. Tesla’s Cybercab tease—unveiled June 2025, already testing in Texas lots.

Industrial? TuSimple’s semis haul freight sans drivers across Arizona. Nuro’s pods deliver groceries in Houston. These aren’t passenger toys; they’re profit machines, lower liability, predictable routes.

Regulatory walls? Crumbling. NHTSA nods to more pilots; Europe’s testing corridors expand. But full L5 autonomy? Still years off outside geo-fences.

One sentence: Scale exposes the cracks.

Is the Hype Finally Matching Reality?

False starts aplenty—Uber’s fatal 2018 crash, Cruise’s SF pedestrian drag. Yet deployments surge. Why now? Data moats deepen; compute explodes (hello, transformer architectures borrowed from LLMs); costs crash.

Skepticism check: Tesla’s “robotaxi” launch? More PR blitz than flawless rollout—early rides needed safety drivers in the shadows. Baidu dominates China, but export? Geopolitics bites.

Unique angle: Watch simulation-to-real gaps. Sims can’t fully mimic rain-slicked leaves or erratic jaywalkers. The map’s AI computing platforms category—Graphcore, Hailo—will bridge that, predicting chaos before it kills.

Bold prediction: By 2030, 20% of urban miles autonomous, but trucks first—cheaper insurance, driver shortages.

Long para time. Enabling tech funds flow to lidar (Ouster raised $150M), but platforms vacuum VC—Waymo’s $5B+ war chest dwarfs startups. Vehicle devs? Partnerships rule: Ford with Argo AI (RIP, acquired by VW). Strategic value? Concentrates in data flywheels. Who controls the trillion-mile datasets owns the models. Tesla leads here, but Waymo’s paid rides forge cleaner signals. China’s Baidu-Pony.ai duo scales fastest, unburdened by U.S. tort law. Regs harmonize slowly—UN’s Vienna Convention updates lag. Investors: bet on platforms with OEM ties (Mobileye-Volkswagen), shun solo sensor bets. Momentum builds where rides happen now.

Why Does This Matter for Investors and Cities?

Cities choke on traffic; robotaxis promise density without gridlock. Investors eye $10T mobility TAM. But antitrust looms—Alphabet, Amazon, Tesla dominating?

Short: Urban planners, take note.

🧬 Related Insights

- Read more: North Korean Hackers Hijack Drift’s Governance, Wipe Out $280 Million in User Funds

- Read more: GetProcessHandleFromHwnd: Windows API’s Lies Fuel UAC Bypasses

Frequently Asked Questions

What companies lead the autonomous driving market?

Waymo, Tesla, Baidu top robotaxis; TuSimple, Nuro for freight. Check enabling like Luminar for sensors.

Is Tesla’s robotaxi service safe and scaling?

Launched June 2025 with geo-fenced tests; millions of FSD miles, but incidents persist—safety drivers nearby.

When will full self-driving be everywhere?

Trucks by 2028, passenger 2030+; regs and edge cases slow L5 rollout outside pilots.