Everyone expected OpenAI to raise money. What nobody expected was the sheer audacity of the number—$852 billion. That’s not a valuation. That’s a bet. A very expensive bet that the company will somehow generate enough revenue to justify a price tag that’s creeping toward some nations’ GDP.

Let’s be clear about what just happened. Amazon, NVIDIA, SoftBank, Microsoft, and a swarm of other institutions threw $122 billion at a company that—despite its cultural dominance—remains wildly unprofitable at scale. The money will go toward “expanded research, product development, infrastructure scaling.” Translation: we need to build more chips to run ChatGPT, train bigger models, and hope that somehow, somewhere, a business model emerges.

The Hype Machine Never Stops

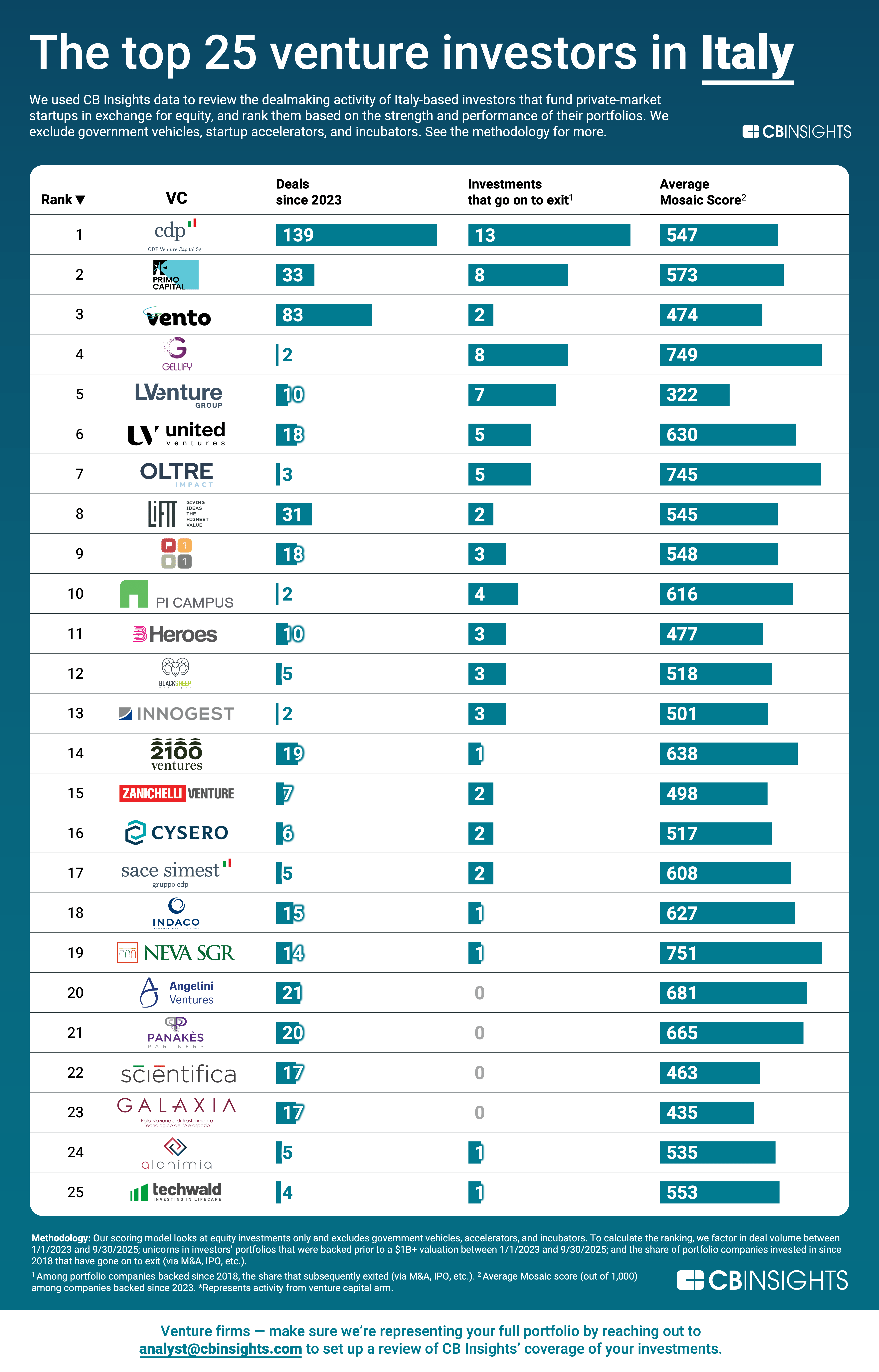

Here’s the thing: we’re living through what might be the most aggressive venture capital goldrush in history. CB Insights reports that private AI companies pulled in roughly $226 billion in 2025—nearly double the year before. PitchBook data shows AI capturing over half of global venture capital deal value in some quarters. These numbers are insane.

But here’s what’s actually happening underneath the euphoria. Capital is concentrating in established players. OpenAI. Anthropic. Startups with recognizable names and founder pedigree. Meanwhile, the entire ecosystem is consolidating around a handful of names. That’s not a healthy market. That’s a casino floor where everyone’s betting on the same horse.

“These figures illustrate sustained investor confidence in the sector’s long-term potential, even as capital flows increasingly favor established players and high-conviction opportunities.”

Notice the language there. “High-conviction opportunities.” In venture speak, that means “places where we’re confident we’ll get returns.” But confidence and returns aren’t the same thing. Confidence is what you have before the IPO. Returns are what you get after it survives its first earnings call.

Is the Money Actually Creating Value?

We need to ask the uncomfortable question here: what problem does OpenAI’s $852 billion valuation solve?

Not the technical problem. OpenAI’s solved that—or at least, they’ve created systems that feel smart. The business problem. OpenAI’s profit margins remain razor-thin because inference costs are brutal. Every time someone asks ChatGPT a question, the company burns cash running GPUs. Their subscription model ($20/month) is a rounding error against that infrastructure bill. Enterprise deals help, but they’re not moving the needle fast enough.

So what’s the $122 billion for? Mostly, it’s a capital arms race. If you don’t spend aggressively on chips and talent, a competitor will. It’s a prisoner’s dilemma dressed up as innovation. Everyone’s forced to keep raising and burning because the alternative—falling behind—is worse.

The fintech and crypto crowds see this differently, of course. They’re convinced AI will “embed itself into core processes like risk assessment, fraud detection, personalized services, and payment optimization.” And sure, that’s probably true at the margins. But margins aren’t revenues. AI-enabled fintech startups command “valuation premiums,” which is just a fancy way of saying people are willing to overpay for them. Premiums compress when the market gets rational.

What Wall Street Isn’t Saying Out Loud

There’s a historical parallel worth digging up here. In the late 1990s, venture capital poured roughly $39 billion into dot-com startups. Adjusted for inflation, that’s about $65 billion in 2024 dollars. We all know how that worked out. Most of those companies vaporized. A handful—Amazon, eBay, Google—became titans. But Google didn’t emerge because it raised more money than its competitors. It won because it had a better algorithm and eventually, a business model.

OpenAI’s situation mirrors this, but with a crucial difference: the “better algorithm” is already built. The question is whether the business model ever arrives. Can you really charge enough for AI services to justify $852 billion? Or are we watching a repeat of 2000—just with GPUs instead of eyeballs?

The broader ecosystem tells a telling story. Juniper Research is forecasting “strong growth trajectories” for conversational and agentic systems in enterprise settings. Notice the weasel words. “Strong growth trajectories.” That’s not a prediction of profitability. That’s a prediction that the market for AI services will get bigger. Markets can get bigger while companies in them go broke.

The Real Play Here

If I’m being honest, the real winner in this arms race isn’t OpenAI. It’s NVIDIA. Every dollar OpenAI raises is a dollar they’ll spend on chips. NVIDIA captures a cut of that infrastructure spend whether OpenAI ever turns a profit or not. Same with Microsoft, which gets equity upside and locks OpenAI into their cloud. These are the actual winners.

OpenAI? They’re the casino. They’re building the house. And the house always wins—until it doesn’t.

What makes this round particularly wild is the sheer confidence behind it. Investors aren’t hedging. They’re not building portfolios of AI bets. They’re doubling down on the handful of names they already know. That’s how you create bubbles. That’s also how you create outsized returns for the few who get it right. But most won’t.

What This Means for Fintech (And Everyone Else)

If you’re building fintech, you’re now competing in an environment where capital is flooding toward “AI-native” solutions. That’s good if you can credibly claim AI makes your product better. That’s terrible if you’re being honest about what AI actually does for you.

The crypto crowd thinks AI + blockchain is the next big thing. Maybe. Probably not in the way they’re imagining. Decentralized computing and tokenized asset management sound great in pitch decks. They sound less great when you realize that “intelligent agents for on-chain activities” is really just algorithmic trading with extra steps.

The Bottom Line

OpenAI’s $122 billion funding round is historically significant. But not for the reasons the press release suggests. It’s significant because it signals that the venture market has stopped asking hard questions. It’s significant because we’re witnessing the consolidation of AI development around a handful of players, which is either the best or worst thing for innovation—depending on your timeline.

The $852 billion valuation? It’ll either look like a bargain in five years, or like the dot-com era redux. Nobody actually knows which. The smart money is betting on the infrastructure plays (NVIDIA, cloud providers) because they have proven business models. OpenAI’s still writing the script.

For now, the funding machine keeps grinding. Models get bigger. Chips get more expensive. And somewhere, a venture capitalist is predicting that AI will “reshape operational models across industries.” Maybe. But reshape them into what? And who pays?

🧬 Related Insights

- Read more: Social Media’s Wild Pivot: Users Become Instant Borrowers Overnight

- Read more: Bitcoin’s Going Nowhere While Altcoins Sprint: Why Your Portfolio Split Matters

Frequently Asked Questions

Will OpenAI’s new funding change my access to ChatGPT? Not immediately. The money goes toward scaling infrastructure and R&D, not product features. Your subscription price might eventually go up, though—someone’s gotta pay for all those GPUs.

Is OpenAI actually making money? No. Not at scale. Their profit margins are deeply negative because inference costs are brutal. They’ve built a product that’s culturally dominant but economically problematic. The funding buys time to fix that.

Will AI startups with OpenAI backing get better returns? Maybe. Or maybe they’ll get crushed by the handful of “high-conviction” players that just absorbed $226 billion in funding. Capital consolidation usually ends in consolidation of outcomes too.