Picture this: Wall Street’s titans, those JPMorgans and BofAs, everyone’s waiting for the next crypto moonshot or AI chatbot to wow the masses. Nah. They’re not playing that game anymore. This week, four big moves from J.P. Morgan, Bank of America, U.S. Bank, and Citi scream one thing—internal systems overhaul. The work beneath the work, as the original piece nails it. Expectations? Shattered.

And here’s the shift: value ain’t in customer-facing apps anymore. It’s buried in ops, data flows, the unglamorous guts that actually make money—or lose it.

Why the Sudden Obsession with Plumbing?

Short answer? They’ve been bleeding. For years. Legacy systems from the ’80s chugging along like rusty V8s in a Tesla world. J.P. Morgan’s kicking it off with their “American Dream Initiative”—sounds noble, right? Targeting small businesses, promising to juice lending to $80 billion over a decade, mentoring 115,000 owners, adding 1,000 bankers. Hands-on stuff.

But peek closer. This isn’t charity. It’s distribution scaling dressed as inclusion. They’re measuring gaps: from 7 million to 10 million small biz clients. Why? Because small biz is where growth hides, and their creaky backends can’t handle the volume without snapping.

“These moves suggest the largest US banks are reorganizing around a thesis: identifying where value is now created and how distant they are from fully internalizing it.”

Spot on. That quote from the original? Pure gold. Banks compete on operations now, not logos.

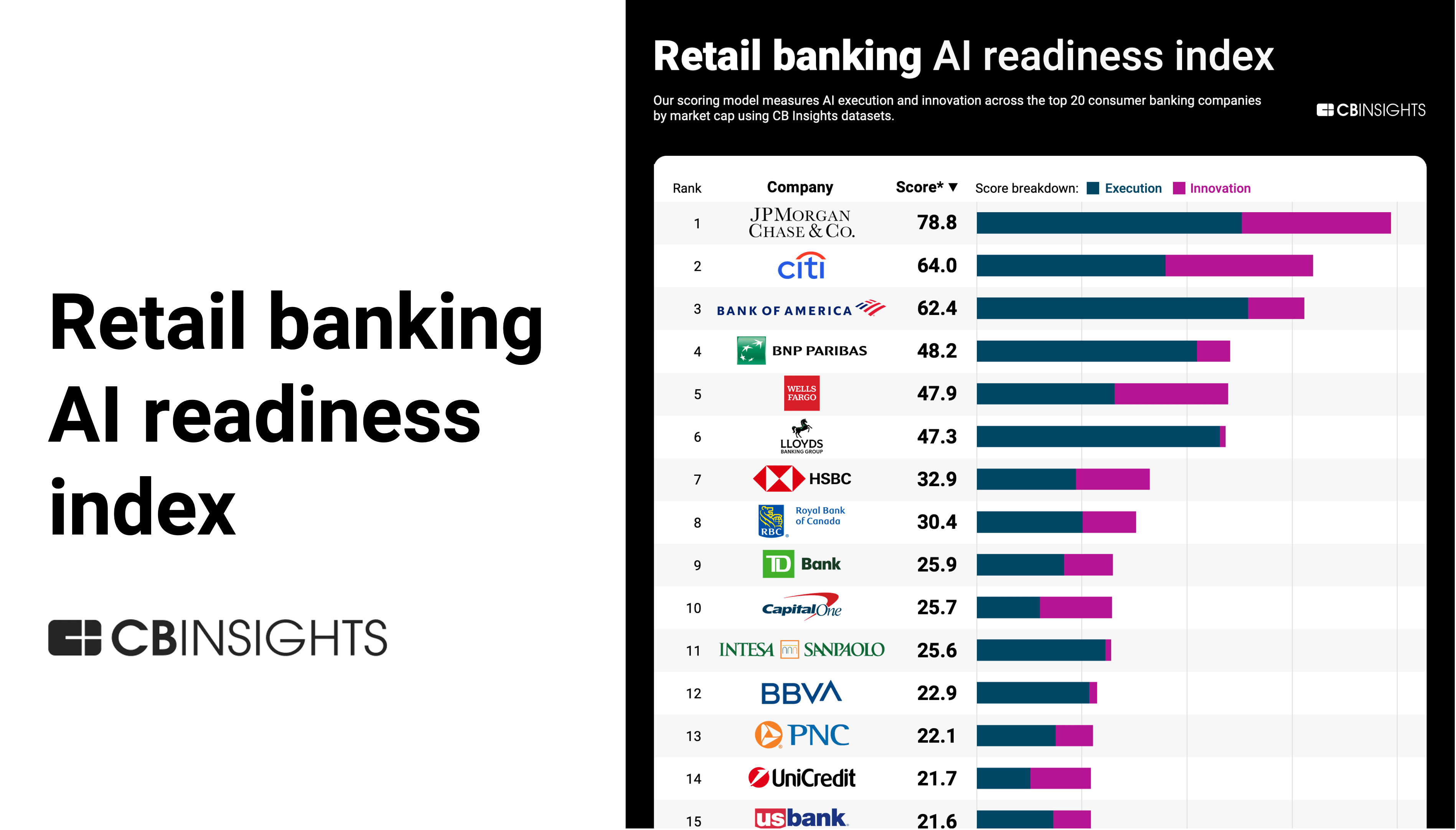

Bank of America? They’re dipping into AI—two developments there, whispers of innovation. Not the hypey kind. Tools to automate compliance, risk scoring. U.S. Bank quashing acquisition rumors—smart, because buying more mess won’t fix internals. Citi? Same playbook, rebuilding pipes for faster everything.

One paragraph wonder: It’s boring. But boring wins.

Is J.P. Morgan’s Small Biz Push Genius or Gimmick?

Look. Everyone loves an underdog story. JPM’s initiative hits six areas, branches swelling with specialists. Doubling senior consultants to 150. Macro weight? Huge, they say.

But—hold up—is this transformative? Or PR spin to mask the real grind: ripping out COBOL dinosaurs for cloud-native stacks? (Yeah, I went there—those 60-year-old languages still haunt banking ledgers.) My unique hot take: this echoes the ’90s Y2K panic. Banks then spent billions modernizing just to not explode. Today? Same vibe, but for AI scale and real-time everything. Prediction: by 2027, the laggards get eaten by fintech natives who’ve always had modern guts.

JPM’s not alone. BofA’s AI tools? Probably agentic workflows for lending approvals—faster, cheaper. No more waiting weeks for a credit check. U.S. Bank’s rumor squash? Focus inward, folks. Citi’s following suit, per reports.

Skeptical? Damn right. Banks love announcing grand plans. Execution? That’s the graveyard.

These aren’t sexy. No viral tweets. But they’re where wars are won. Operations determine if you survive the next downturn—or thrive.

What About the AI Angle—Real or Hype?

Two of the four moves: AI innovation. BofA leading, likely. Tools for what? Fraud detection? Personalized lending? The original lumps ‘em together, but dig: it’s internal. Not customer-facing chatbots. Think: AI optimizing capital allocation, predicting defaults before they hit.

Here’s the dry humor: banks discovering AI like Columbus ‘found’ America. They’ve had the data forever—petabytes rotting in silos. Now, finally, pipelines to feed it.

But call out the spin. “Innovation,” they trumpet. Really? It’s catch-up. Fintechs like Chime, SoFi built AI-first. Big banks? Retrofitting.

Paragraph sprawl time: And while regulators circle—hello, CFPB on AI bias—these overhauls mean modular systems, easier audits, swappable models. Comma after comma, it weaves compliance into agility, compares to old monolithic mainframes that took months to patch, lands here: without this, they’re dinosaurs waiting for the asteroid.

USB’s rumor kill? Brilliant. Acquiring more legacy? Madness. Better rebuild solo.

The Hidden Cost: Talent Wars and Billions Burned

Don’t kid yourself. This costs a fortune. JPM’s banker hires alone? Millions in salaries. Tech talent? Worse—devs who know banking regs and modern stacks are unicorns.

Opinion: they’re poaching from Big Tech, offering stability for misery. (Gold handcuffs, anyone?) Historical parallel—remember Knight Capital’s 2012 algo glitch? $440 million gone in minutes due to bad code. Internal rebuilds prevent that. Bold prediction: first bank to fully modernize wins 20% margins in lending.

Citi’s play? Similar—streamlining global ops. Global means headaches. Time zones, regs. AI helps, but only if pipes flow.

Short. Brutal. True.

So, changes everything? Potentially. If they deliver. Expectations were fintech takeovers. Reality: incumbents fortifying castles.

🧬 Related Insights

- Read more: Agentic AI’s 2026 Scale-Up Nightmares: 5 Roadblocks Killing Prototypes

- Read more: Amazon’s Ruthless Price Squeeze: Brands Like Adidas Bolt for the Exits

Frequently Asked Questions

What is J.P. Morgan’s American Dream Initiative?

JPM’s plan to support 10 million small businesses with $80B lending, mentoring, and 1,000 new bankers over a decade—aimed at growth, not just PR.

Why are big banks rebuilding internal systems now?

Legacy tech can’t handle AI, real-time data, or scale—value’s in ops, not apps, so they’re measuring and closing gaps.

Will this make banks more competitive against fintechs?

Maybe—if they execute. Modern guts mean speed and cost wins; laggards get disrupted.