Pilots grounded. Procurement soars.

Oil & gas companies aren’t tinkering anymore. They’re buying. Across the oil & gas value chain market map, 235 high-potential firms — screened by Mosaic scores over 500 and ESP rankings — are shifting tech from experimental side-projects to core infrastructure. Aging control systems creak under pressure, emissions regs bite harder, and modular designs shrink carbon capture footprints. It’s not hype; it’s happening.

And here’s the kicker: AI and gen AI? They snag less than 20% of US oil & gas IT budgets now. But projections? Over 50% by 2029. EPA’s nod to autonomous drones slashes red tape for inspections. Incumbents scramble, snapping up software-defined automation. Why? Operational snarls multiply, regs tighten — early movers snag efficiency and compliance edges.

Why This Oil & Gas Value Chain Market Map Matters Now

Look, energy’s black gold has always been analog at heart — rusty rigs, gut-feel decisions. But underlying architecture flips. Legacy SCADA crumbles; software eats the world, even pipelines.

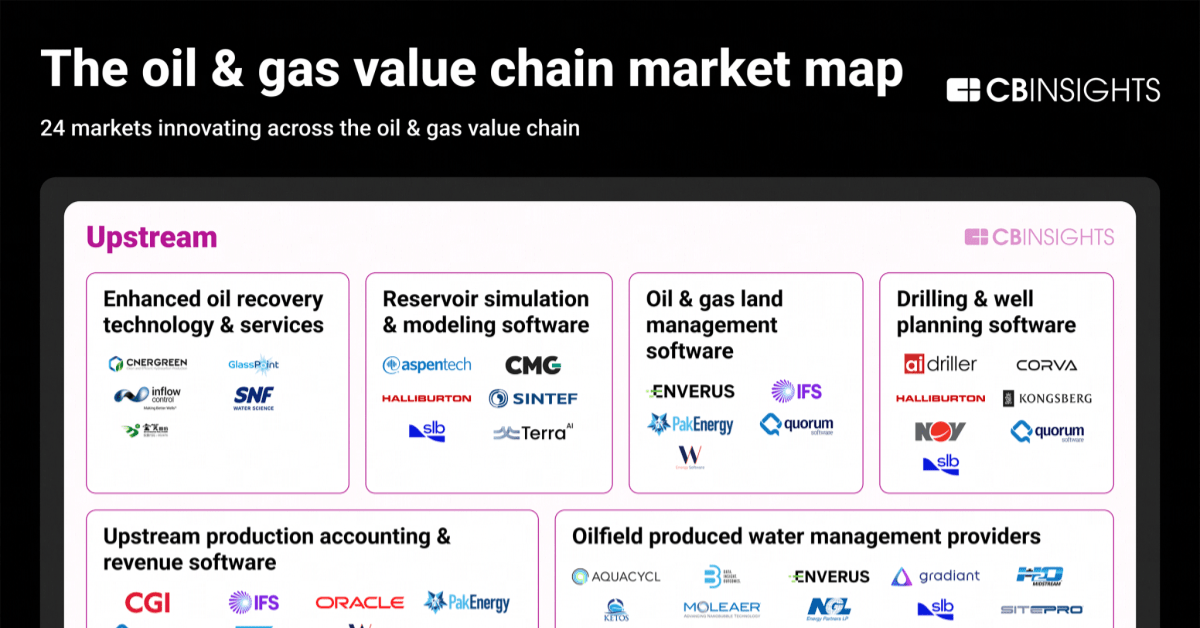

We sliced it into four layers: upstream (exploration to production), midstream (pipes and tanks), downstream (refining to pumps), and horizontal (cross-cut enablers). Each packs dozens of winners, vetted on hiring velocity, score growth, partnerships, exit odds.

Take upstream. Reservoir sims, enhanced recovery, produced water tech. These aren’t bolt-ons; they’re rearchitecting reservoirs as data meshes.

Short para: Midstream’s where leaks kill.

How Upstream Tech Drills Smarter, Deeper

Reservoir simulation used to mean supercomputers in basements — slow, siloed. Now? Cloud-native twins predict flows in real-time, blending seismic data with gen AI for what-if scenarios. Drilling? Well planning software optimizes bits before steel hits rock, cutting non-productive time by 30% sometimes.

Produced water — that salty nightmare from fracks — gets treated modularly, membranes and AI-optimized electrolysis slashing disposal costs. Land management? GIS fused with satellite feeds tracks leases, regs, even ESG scores.

But my unique angle: this echoes the PC revolution in 80s manufacturing. Then, spreadsheets killed mainframes; now, AI agents kill manual logs. Bold call — upstream autonomy hits 40% of ops by 2028, forcing Big Oil to spin out software arms.

AI and gen AI currently account for less than 20% of total IT spending by US oil & gas companies, but that share is expected to exceed 50% by 2029.

Is Midstream the Silent Efficiency Killer?

Pipelines span thousands of miles — invisible until they rupture. Enter fiber-optic sensing, glued along lines, vibrating alerts for digs or leaks before booms. SCADA evolves to edge AI, predicting pressures sans constant human eyes.

Terminal platforms juggle throughput; tank integrity uses ultrasonics and drones for wall scans. Why now? Methane rules from EPA demand it — fines sting worse than upgrades.

Here’s the thing — midstream’s bottleneck status? It’s architectural. Legacy pipes can’t flex for LNG booms or hydrogen blends. These 50+ mapped firms modularize monitoring, turning iron veins into smart grids.

Downstream: Refineries Go Digital or Die

Refining’s alchemy — crude to gasoline — swims in variables: feedstock swings, yield tweaks. Process sims now gen AI-boosted, optimizing crackers in silico. Planning tools forecast margins blending weather, geopolitics, crack spreads.

Distribution? Wholesale platforms match trucks to tanks dynamically. Retail? Fuel management dials pumps via IoT, sniffing demand from EV creep.

Skeptical note: Big Refiner PR spins ‘digital twins’ as savior, but it’s often repackaged ERP. Real shift? Open APIs linking sims to trading floors.

Horizontal Tech: The Glue Across Chains

These cross-cutters — 100+ firms — wield the real power. Industrial IoT platforms federate sensors chain-wide. Drones and sats spot flares, methane plumes. Engineering sims (CFD on steroids) design everything modular.

Asset management? Predictive twins flag failures. Energy trading platforms? AI arbitrage volatility. Emissions? CCUS stacks, now Lego-like, stackable on any site.

Prediction I don’t see elsewhere: horizontals birth ‘energy OS’ — unified stacks where oil firms plug in like apps. Exxon as app store? Watch it.

And emissions — tightening noose. But modular CCUS (direct air capture mini-plants) flips script: oil funds green tech, leading net-zero ironically.

Why Does This Reshape Energy’s Future?

Complexity explodes — net-zero mandates, volatile prices, talent droughts. Winners? Those weaving automation, monitoring, modularity early.

Trends scream: hiring in AI/ML spikes 3x peers. Mosaic growth? Top quartile firms up 25% YoY. Partnerships? Verticals mash with hyperscalers.

Corporate spin calls it ‘transformation’; it’s survival. Laggards face stranded assets.

🧬 Related Insights

- Read more: Excalidraw: The No-BS Whiteboard That Keeps Your Sketches Private

- Read more: Anthology’s Backstory Trick: Making AI Mimic Real Humans, One Life Story at a Time

Frequently Asked Questions

What is the oil & gas value chain market map?

A breakdown of 235 top tech firms across upstream, midstream, downstream, and horizontal layers, scored for success potential.

How is AI changing oil & gas operations?

From <20% to >50% IT spend by 2029, powering sims, predictions, autonomous inspections.

Will oil & gas tech go green faster?

Yes — modular CCUS and monitoring enforce emissions compliance, positioning early adopters as low-carbon leaders.