What if the real battleground for agentic commerce isn’t AI capability—it’s payment plumbing?

That’s the quiet revolution unfolding at Stripe right now. While everyone obsesses over whether Claude can book your flight better than you can, the company is systematically solving a harder, less glamorous problem: how do AI agents actually pay for things without storing your financial secrets?

The answer, it turns out, is Shared Payment Tokens (SPTs)—and Stripe just made them dramatically more powerful.

The Token That Changes Everything

Last year, Stripe introduced SPTs as a payment primitive designed specifically for agentic commerce. Picture this: your shopping AI asks permission once. You grant it. From then on, the agent can transact autonomously using a scoped, one-time credential—a digital token tied to your intent but not to your actual card details. No exposing your 16-digit number. No token stuffing. No persistent card-on-file vulnerability.

It worked. Etsy, Urban Outfitters, Anthropologie, Free People all adopted it. But sellers came back asking the obvious question: what about the payment methods my customers actually use?

Why This Timing Matters (And Why You Missed It)

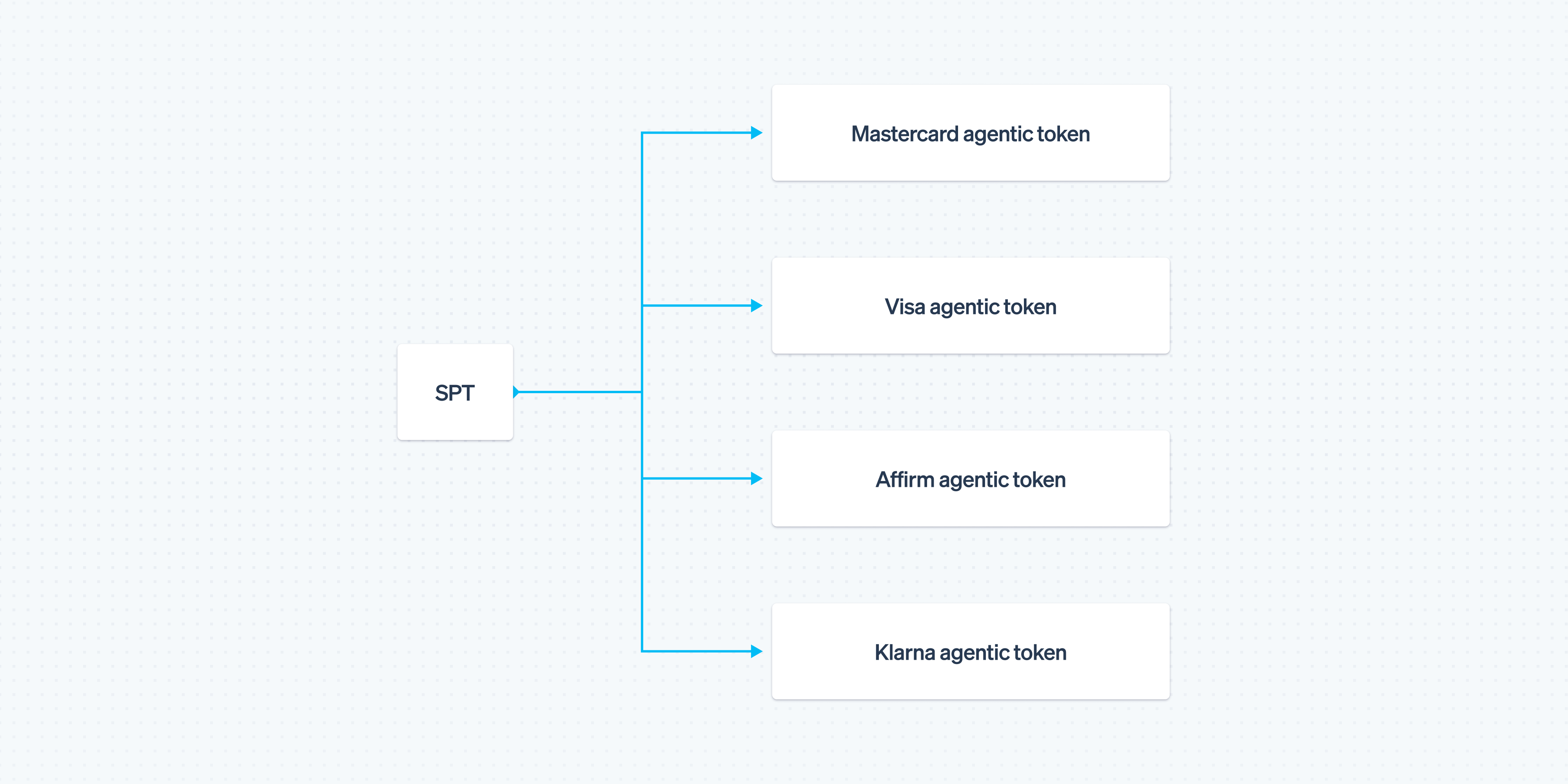

Stripe just announced support for something that sounds boring but is architecturally wild: agentic network tokens from Mastercard and Visa, plus BNPL tokens from Affirm and Klarna.

Here’s what’s actually happening beneath the marketing language.

For years, payment networks (Mastercard, Visa) have issued “network tokens”—these are secure digital stand-ins for physical cards that merchants can vault and reuse. Stripe’s innovation wasn’t inventing tokens. It was asking: what if we issued network tokens specifically designed for AI agents? Scoped to customer intent. Temporary. Revocable.

Mastercard and Visa listened. They built Agent Pay and Intelligent Commerce—which are just fancy names for “network tokens that speak agent protocol.” Stripe integrated them into SPTs.

The result? This is now the only platform where a seller can offer an agent access to a Visa network token and a Klarna BNPL option through a single API primitive. That’s not just convenience—that’s architectural consolidation. That’s what happens when an infrastructure layer matures.

“Agentic commerce is accelerating the next phase of digital payments, where security, control, and scale are foundational,” said Rubail Birwadker, senior vice president at Visa.

How This Actually Works (The Unsexy But Important Part)

Let’s walk through the mechanics, because this is where you see the real engineering.

A customer tells an AI agent: “Book me a flight and pay with my Visa if you can get a good deal.” The customer’s bank (the issuer) creates a token scoped to that intent—a credential that exists only for flight purchases, only with this merchant, only for the next 24 hours. Stripe provisions it, hands it to the agent. The agent flies through five airline websites. At each one, it presents the token. Visa’s network automatically maps it back to the customer’s real FPAN (Funding Primary Account Number), verifies it’s still valid, checks it hasn’t been revoked, and approves it.

For the issuer, this is better than traditional card-on-file because they see why the agent is charging—the authorization includes metadata about customer intent. For fraud detection, that’s gold. For the customer, the token expires or revokes instantly if they want it to.

Now add BNPL. Customer picks Klarna. Stripe surfaces Klarna’s confirmation UI to the agent without exposing Klarna credentials to Stripe. The agent shows the customer “pay in 4 installments” and the customer confirms directly with Klarna. No middleware complexity.

The Bigger Picture: Why Payments Infrastructure Is Becoming the Real Moat

Everyone’s focused on whether GPT-5 or Claude 4 will out-reason their competitor. But the actual bottleneck for agentic commerce isn’t thinking—it’s trust.

Who do you trust your payment method with? That’s the question. And the answer used to be: whoever has a PCI-compliant vault. Now it’s: whoever has a token I can revoke, scope, and understand.

Stripe is building the scaffolding that makes that trust possible. They’re not trying to be the payment network. They’re becoming the layer that translates between customer intent, agent capability, and network infrastructure. That’s a defensible position—and it’s how platforms become essential.

The BNPL expansion is particularly smart. BNPL accounts for over $300 billion in transactions globally, and merchants see a 14% revenue lift on BNPL-eligible sessions. But most BNPL APIs were built for humans clicking checkout buttons, not for agents running autonomous purchase loops. Stripe rewired it.

Is This the End of Payment Diversity?

Not quite. But Stripe just became the only provider with a unified API surface for network tokens and alternative payment methods in agentic flows. That’s a first-mover advantage that compounds—because integrating five payment methods separately is annoying, but integrating them through one primitive is elegant.

The risk? If Stripe stumbles on security, interoperability, or pricing, competitors could exploit it. But right now, they’ve pulled ahead on a layer most startups aren’t even thinking about yet.

The agentic economy isn’t coming. It’s here, operating at scale through Etsy and Urban Outfitters, and the payments infrastructure is quietly reshaping itself to support it. Stripe saw that shift earlier than anyone else.

🧬 Related Insights

- Read more: Coinbase’s AI Payments Protocol x402 Just Got the Tech Giants’ Blessing—Here’s Why It Matters

- Read more: Bitcoin’s Going Nowhere While Altcoins Sprint: Why Your Portfolio Split Matters

Frequently Asked Questions

What is an agentic network token and how is it different from a regular network token? An agentic network token is scoped to a specific customer intent and transaction type, and is designed for AI agents to use autonomously. Regular network tokens are typically broader and usually require per-transaction authorization. Agentic tokens let customers grant permission once and let the agent execute multiple purchases within that scope.

Will I have to do anything special as a Stripe customer to support these new payment methods? No. If you’re already processing payments with Stripe and using SPTs, Mastercard Agent Pay, Visa Intelligent Commerce, Affirm, and Klarna support is automatically available for agentic transactions. Stripe handles the complexity of provisioning and routing behind the scenes.

Does this mean my credit card information gets shared with AI agents? No—that’s the entire point. The agent never sees your card number. It only receives a temporary, scoped token that’s tied to your intent and can be revoked instantly. The payment network handles the credential translation between the token and your actual account.