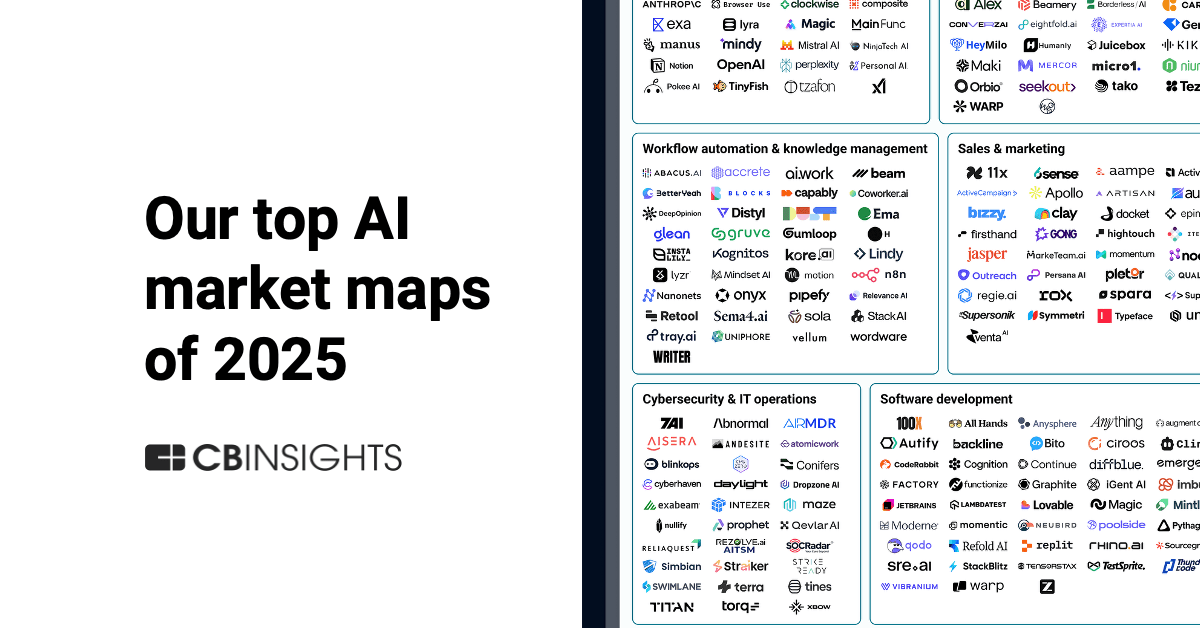

Agents everywhere. That’s the scene right now—1,000-plus agentic AI offerings flooding the market, each swearing it’ll rewrite software’s future.

CB Insights drops their top AI market maps of 2025, and it’s a battlefield snapshot: agent platforms duking it out, infrastructure groaning under compute demands, vertical apps infiltrating factories and hospitals. No fluff. Just data on who’s pulling ahead.

Zoom out. The foundation model frenzy? It’s splintering. Horizontal plays like coding agents snag quick cash—multiple outfits already at $100M+ ARR. But here’s the pivot: specialization’s the new king. We’re talking tailored agents for niches that bleed real revenue.

“2025 saw the emergence of 1,000+ agentic AI offerings promising the next evolution of software. While horizontal applications such as coding have quickly gained commercial traction with multiple companies generating 100M+ ARR, the market is moving toward greater industry specialization.”

That’s CB Insights nailing it. Spot on.

Why AI Infrastructure Feels Like a Ticking Bomb

Data centers. Multi-gigawatt beasts sprouting up, enough juice to light a city. AI’s hunger is real—power bottlenecks sparking wild innovation everywhere from chips to cooling.

But wait. This echoes the PC boom of the ’80s (my unique angle here): back then, app developers raced ahead while Intel and Microsoft muscled infrastructure. Today? Nvidia owns semis, but utilities can’t keep up. Expect blackouts—or winners who crack nuclear micro-reactors first. Hype says endless scaling. Data screams limits.

Short para for punch: Power wins markets.

Infrastructure maps highlight it: every layer from hyperscalers to edge providers racing to plug the gap. Yet CB Insights flags the crunch—buildouts lag training needs by years.

And the editorial take? Betting big on infra without power fixes is Wall Street’s next bagholder play. Skeptical? Damn right. Numbers don’t lie.

Humanoids in Warehouses: Sci-Fi or Supply Chain Savior?

Shift to physical ops. Humanoid robots storming factories, automated warehouses humming. CB Insights maps 280 AI firms bulldozing construction dinosaurs.

Physical ops isn’t chatbots. It’s torque, sensors, real-world chaos. Tesla’s Optimus? Early buzz. But Figure AI and Boston Dynamics edge ahead on deployments—per the maps.

Look, retail’s next: shelves restocked by bots, not bored teens. Government? Drones for disaster response. These verticals aren’t moonshots; they’re ROI machines as labor costs spike.

Is Healthcare’s AI Makeover All It’s Cracked Up to Be?

GenAI crashes clinical ops. Drug discovery timelines slashed—think months, not years. CB Insights’ Digital Health 50 ranks the disruptors: startups blending models with patient data for precision plays.

But here’s the rub (parenthetical skepticism): regulatory moats are thick. FDA approvals? Still a slog. Maps show promise—Figure AI in robotics parallels here—but overhyping “reshaping” ignores compliance walls.

Life sciences vertical? Booming. Yet my bold prediction: without federated learning breakthroughs, data silos kill the party by 2027.

Retail and government get nods too—personalized pricing algos, predictive policing. Sprawling? Sure. But maps tie it to ARR trajectories, not vaporware.

Flagship rankings seal the deal. AI 100: hottest startups per CB’s predictive mojo. Fintech 100, Insurtech 50—crossovers everywhere. It’s not random; Mosaic scores crunch patents, talent poaches, funding velocity.

One para wonder: Winners emerge where agents meet atoms.

So, strategy verdict? Chase specialized agents and infra innovators. Broad bets flop in power-starved 2026.

Dense dive: Healthcare’s edge comes from vertical depth—CB’s Digital Health 50 spotlights 50 firms with clinical pilots live. Insurtech? Claims automation via agents hits 30% efficiency gains already. Fintech 100 blends LLMs with blockchain for fraud nets that actually work. Government apps? Less sexy, more steady—think permitting bots slashing backlogs. Physical ops maps (humanoids, warehouses, construction) scream opportunity: labor shortages + AI = trillion-dollar TAM. Infrastructure? The silent killer—multi-GW builds, but grid constraints cap hyperscalers at 20% utilization spikes. Agents? 1,000+ offerings, but only 10% hit product-market fit per traction data.

My sharp position: These maps aren’t cheerleading. They’re battle plans. Ignore power at your peril—it’s the ’80s chip shortage redux, dooming half these unicorns.

What Sets 2025’s Leaders Apart?

CB’s predictive intelligence isn’t tea leaves. It’s ML on 10M+ data points: momentum scores blending web buzz, partner deals, exec pedigrees.

Take AI 100. Top tier? Agent builders with vertical hooks. Not generalists.

Short and sharp: Data crowns specialists.

Frequently Asked Questions

What are CB Insights’ top AI market maps for 2025?

They cover AI agents, infrastructure, physical ops (humanoids, warehouses), healthcare, retail, government—plus ranked lists like AI 100.

Which AI startups are most promising in 2025?

CB’s AI 100, Fintech 100, Digital Health 50, Insurtech 50—scored on patents, funding, traction.

Will power shortages kill AI growth in 2025?

Maps show massive builds, but bottlenecks loom—innovation in energy (e.g., SMRs) decides winners.