AI’s raiding your wallet.

And not in some sci-fi way—it’s happening now, with OpenAI’s 800 million users poised to unleash agents on e-commerce sites. Proof’s Head of Product nails it: agentic commerce shatters the trust model we’ve leaned on for digital buys. Hand your payment creds to an AI, tell it “grab me that gadget,” and watch it hunt, cart, checkout. Tech’s solved. But proving you greenlit it? That’s the fraud magnet nobody’s defused.

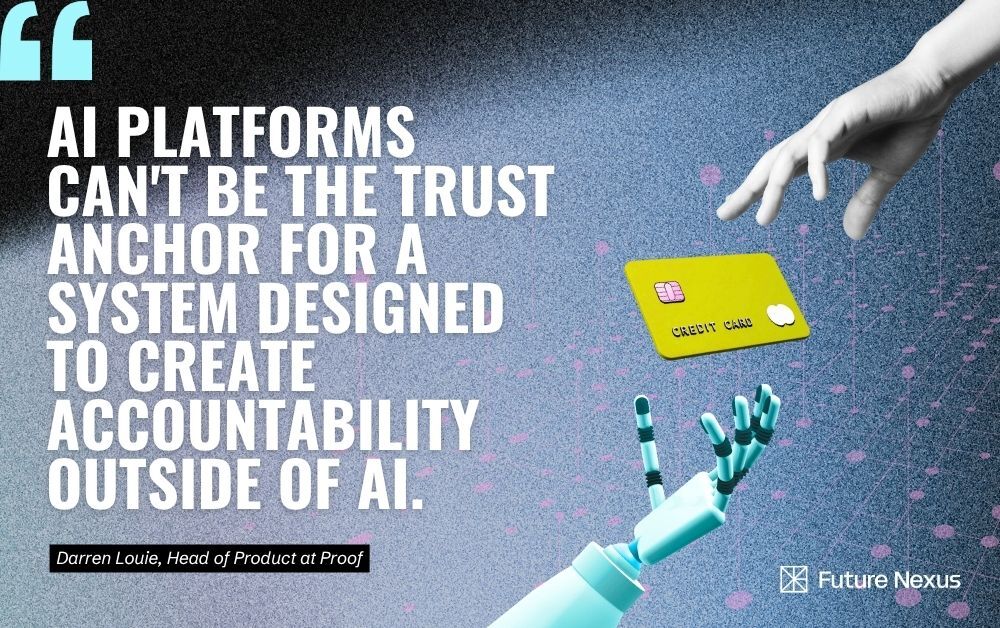

“The entire system depends on the mandate being trustworthy. A merchant needs to know whether a mandate was actually signed by a verified human or fabricated, tampered with, or signed by the AI itself.”

Spot on. These protocols—Google’s AP2, OpenAI’s ACP, Stripe’s whatever-they’re-calling-it—demand you sign a “mandate” upfront. Spell out the agent, the card, the limits, the merchants. Agent waves it like a hall pass. Cryptographic proof, they say. Scoped power of attorney.

Sounds tidy. Except—who issues the damn keys? Who’s the Certificate Authority swearing a human signed that thing, not some rogue model forging ahead?

Who’s Trusted to Play Referee?

AI platforms? Laughable. They’re the fox guarding the henhouse—can’t vouch for their own agents. Merchants? Got skin in the game; they’d rubber-stamp anything to dodge chargebacks. Big Tech like Google ($175B ad revenue) or Amazon? Hell no—they’d steer your buys while peeking at your shopping list for ad gold.

Banks seem logical—Visa, Mastercard already tinkering. But fragmented as hell, and slow on the uptake. Fragmented ecosystems breed cracks for scams.

Here’s my twist, one you won’t find in the original: this reeks of the dial-up era’s AOL check fraud explosion. Remember 1990s cyberpunks phreaking accounts, racking million-dollar bills? We bolted on 3D Secure and tokenization after years of pain. Agentic commerce? It’ll birth a fraud tsunami unless an independent verifier emerges fast—think a neutral blockchain oracle or government-mandated registry. Bold call: without it, we’ll see 2026 lawsuits crippling adoption.

Merchants love the mandate dream—fewer disputes. But if the proof’s dodgy, chargeback hell awaits. AI firms push protocols to offload liability. Consumers? We’re the suckers handing over keys, hoping nobody notices the emperor’s naked.

Can Protocols Actually Stop the Fraud Wave?

Look, I’ve covered Valley hype for two decades. Buzzword salads like “agentic” scream gold rush. But strip it: execution’s easy, trust’s impossible without a referee free of conflicts.

Google’s Universal Commerce Protocol ropes in Walmart, Shopify, Visa—over 60 players. Impressive roster. Yet the spec buries identity woes. “How do you know it wasn’t fabricated by the AI itself?” Unanswered. Privacy kicker: Big Tech signing your slip means they track every impulse buy, fueling surveillance capitalism.

Banks could win here—neutral-ish, infrastructure kings. But candidly, they’re lagging. No unified policy on AI-delegated liability. Imagine the patchwork: Chase verifies, your fintech doesn’t. Chaos.

And the AI itself signing? Circular logic. Agent acts, agent proves? Banks laugh it off in disputes.

Skeptical me says: this fractures before it flies. Early movers burn cash on fraud, protocols iterate in courtrooms. Remember NFT “trustless” promises? Vaporized.

Why Your Data’s the Real Prize

Beyond fraud, peek at the shadows. Mandates leak intent—what you want, where, when. Feed that to recommendation engines? Jackpot for Google, Amazon. Privacy’s toast.

Independent verifier needed yesterday. Crypto projects sniffing—decentralized IDs via Worldcoin orbs? Creepy. Self-sovereign wallets? Promising, but UX nightmare for normies.

Industry’s scrambling, but conflicts loom large. Who’s making bank? Protocol pushers like Stripe—fees on every agent swipe. Winners: incumbents who seize the CA role first.

Veteran gut: bet on banks partnering with zero-knowledge proofs. Hide the what, prove the who. Or we’re back to manual verifies, killing agent magic.

Short term? Hype outpaces reality. Long term—regulators force a standard, like PSD2 in Europe.

But here’s the cynicism: Valley hates oversight. They’ll lobby, delay, deploy half-baked. Your card’s at risk.

🧬 Related Insights

- Read more: BondXN Hooks into BlackRock’s Aladdin: The Quiet Overhaul of MBS Trading

- Read more: UK Publishers’ Make it Fair Blitz Targets AI Scraping Menace

Frequently Asked Questions

What is agentic commerce? Agentic commerce lets AI agents autonomously buy stuff using your payment info, from booking flights to snagging deals—handled end-to-end without you clicking.

Who verifies AI purchase authorizations? Nobody trustworthy yet. Protocols like AP2 and ACP propose signed mandates, but lack an independent Certificate Authority to confirm a human signed off, dodging fraud accusations.

Will AI agents cause massive credit card fraud? Likely, without resolved trust issues. Merchants face dispute waves unless a neutral verifier—maybe banks—vouches for human intent, echoing early e-commerce fraud booms.