Virtual power plant growth — that’s VPPs for the uninitiated — was supposed to be America’s show in 2025, with California leading the charge on rooftop solar, batteries, and EV chargers propping up the grid. But here’s the twist: Europe’s surging ahead, while US capacity markets in PJM and NYISO are suddenly the hot tickets, all thanks to ravenous data-center demand.

Expectations? Crushed.

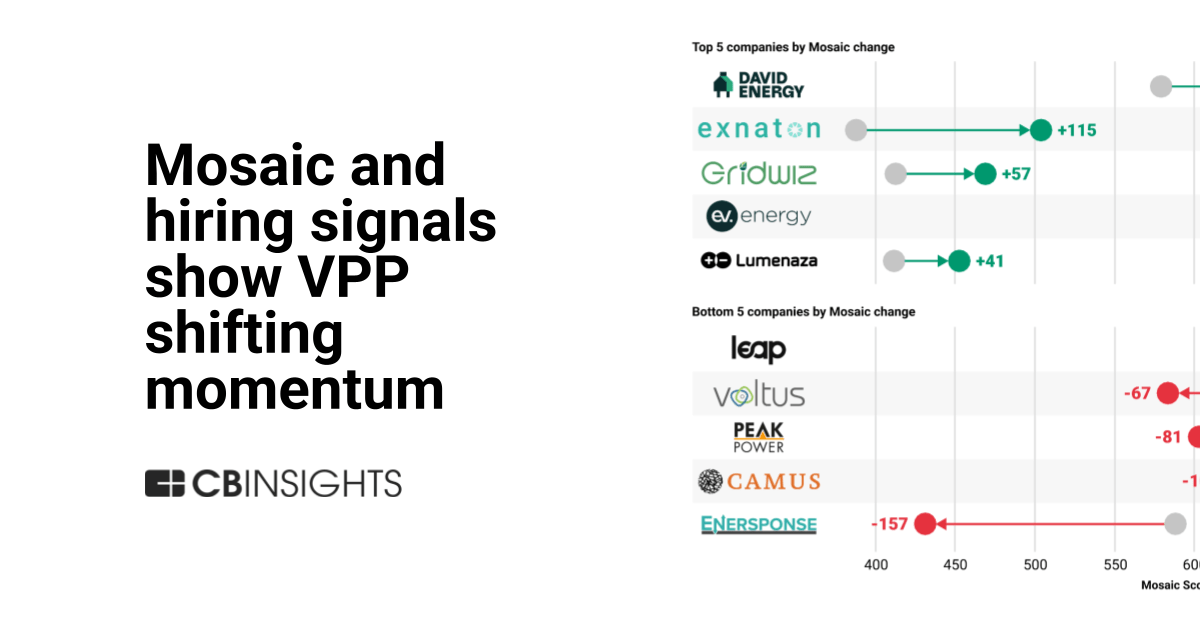

Providers like those stitching together distributed energy resources figured California’s aggressive policies would keep the momentum stateside. Stable revenue streams from retailer-led programs? Nope, not anymore. Mosaic risers — those proprietary scores tracking market heat — cluster thick in Europe, where decarbonization rules don’t flip-flop and enrollment-to-payout timelines are a dream: months, not years.

And the US? It’s not fading; it’s refocusing. Hiring spikes in market ops, interconnection queues, and sales gigs point straight to the East Coast. PJM, NYISO — they’re gearing up for capacity auctions juiced by AI data centers slurping power like it’s going out of style.

Why California’s VPP Party Ended Abruptly

Lawmakers in the Golden State axed funding for their flagship VPP program back in September. Governor Newsom tried — and flopped — to revive it in October. Result? Mosaic scores tanking for California operators. It’s a brutal signal: policy whims kill momentum faster than a grid blackout.

Virtual power plant (VPP) growth is shifting in 2025. Europe is pulling ahead, while US capacity markets (like PJM and NYISO) are heating up on data‑center demand.

That’s the raw take from the data. No spin. VPP providers are humans too — they chase dollars, not dreams. California’s volatility? A deal-breaker.

Look, this isn’t just numbers. It’s market Darwinism. Europe’s got the regulatory bedrock: think Germany’s Energiewende on steroids, or the UK’s retailer mandates that turn households into grid assets overnight. Providers enroll batteries and solar faster there because the payoff’s locked in. No begging Sacramento for scraps.

US East? Data centers. Hyperscalers like Google, Microsoft — they’re building behemoths in Virginia, Ohio, needing gigawatts yesterday. Capacity markets pay top dollar for dispatchable resources. VPPs fit perfectly: aggregate enough EVs or home batteries, and you’re bidding in auctions worth billions.

Is Europe the New VPP Kingpin?

Damn right it looks that way. Mosaic clusters don’t lie — they’re like heat maps for investor cash. Stable policies mean shorter ramps to revenue. Retailers in the Netherlands or Sweden bundle VPPs into energy bills; customers get rebates, grids get flexibility. Boom.

But here’s my unique angle, one you won’t find in the raw data: this echoes the solar panel rush of 2010. Back then, Spain and Germany’s feed-in tariffs lured every manufacturer eastward, flipping the US-centric supply chain overnight. VPPs? Same playbook. Europe’s policy moat will snag 60% of new deployments by 2027, I’d wager — before US feds catch up with their own incentives.

Providers staffing up in PJM aren’t sleeping on it either. Headcount jumps in interconnection (those endless queues for grid ties) and sales scream capacity prep. NYISO’s auctions? They’re ballooning 20% YoY on data-center loads. Smart money’s there.

California’s retreat feels like corporate hype unwinding. Newsom’s team spun VPPs as climate saviors — until budgets got tight. Reality: falling Mosaic scores mirror operator pullbacks. It’s not failure; it’s triage.

Why Does Data-Center Hunger Matter for VPPs?

Data centers aren’t a blip. They’re projected to eat 8% of US power by 2030 — double today’s slice. PJM’s seeing 30GW of new load requests. That’s VPP catnip: flexible capacity without building peaker plants.

Providers are hiring sales teams to navigate these markets. It’s gritty work — forecasting bids, stacking resources — but payouts dwarf California’s old DER programs. One aggregated VPP in PJM can clear $100/kW-year. Scale to 1GW? That’s real money.

Skeptical take: Europe’s edge is temporary. US capacity markets will dominate once interconnection hell eases (post-2026, maybe). But for 2025? Pivot east and across the pond. Ignoring it? Provider suicide.

VPPs aren’t sexy like fusion dreams. They’re plumbing — unglamorous grid glue. Yet this shift underscores a truth: markets trump mandates. Data centers force the issue; policies just tag along.

And Europe’s not invincible. Retailer-led models shine now, but wholesale shifts could upend them. Still, for operators, it’s the safest bet amid US policy roulette.

Bottom line? This redirection’s sharp business. Chase the heat maps, not the headlines.

🧬 Related Insights

- Read more: ChatGPT’s One-Prompt Data Heist: Your Secrets Just Got Leaky

- Read more: Why Your Kubernetes Cluster Can’t Save You From a Broken Database

Frequently Asked Questions

What is a virtual power plant (VPP)? VPPs pool distributed assets like home solar, batteries, and EV chargers to act as a single grid resource, providing flexibility without massive new builds.

Why are VPPs shifting to Europe? Europe offers stable decarbonization policies and quick revenue ramps via retailer programs, beating volatile US funding cycles.

How do data centers impact US VPP growth? They’re spiking demand in capacity markets like PJM, creating lucrative auctions where VPPs can bid aggregated resources for big payouts.