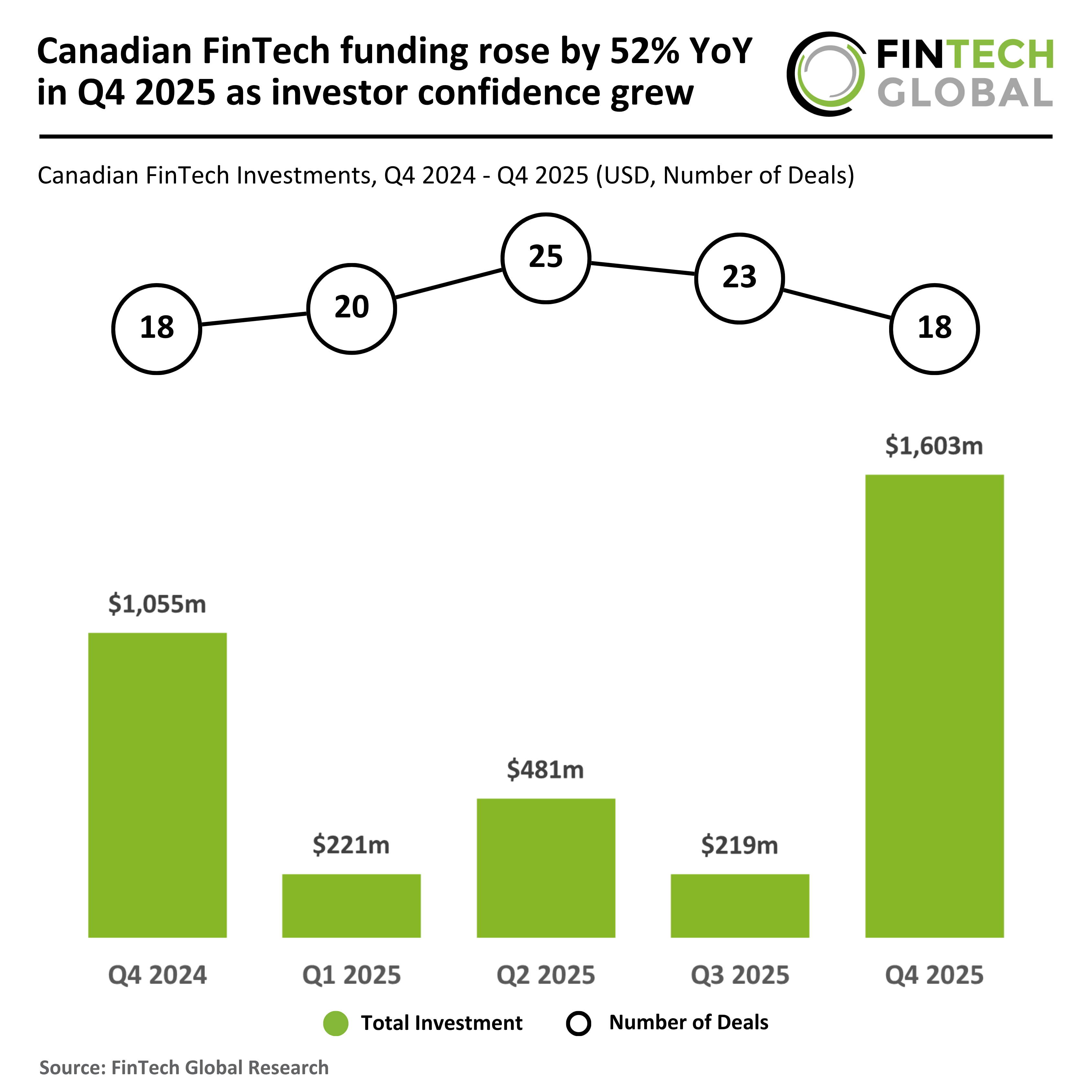

Everyone was waiting for a sign. After a brutal 2024 for venture capital, the tech sector spent most of 2025 holding its breath. Q3 was particularly rough—Canadian FinTech pulled in just $219.3m across 23 deals, an embarrassing $9.5m per transaction. The sector looked dead money. Then Q4 happened, and suddenly the narrative flipped on its head.

Canadian FinTech funding rose 52% year-over-year in Q4 2025, landing at $1.6 billion across 18 transactions. But here’s what everyone’s getting wrong about these numbers: it’s not really about the volume of deals. It’s about the size of the bet.

The Deal Size Explosion Nobody’s Talking About

Average deal value jumped to $89.1m per transaction in Q4 2025. That’s a 34% jump from Q4 2024’s $58.6m average—and when you stack it against Q3’s pathetic $9.5m mean, you’re looking at a roughly tenfold increase in conviction per check written.

This matters because it signals something deeper than just holiday-season capital deployment. Investors aren’t writing more checks. They’re writing bigger checks. The composition of the market fundamentally shifted. Fewer, fatter deals. That’s a sign of confidence, sure, but also of consolidation and selectivity. Weaker FinTechs are getting squeezed out. Winners are getting validated.

“Average deal value increased to $89.1m as investors demonstrated greater confidence in the market,” according to the quarterly data.

What’s wild is that Q4 2025 crushed Q3 despite having five fewer deals (18 vs. 23). That’s the real headline. You don’t need deal volume when individual deals are 9.4x bigger.

Why Does This Matter for Canadian FinTech’s Future?

Canada has always played second fiddle to the U.S. in fintech. The sector’s been perpetually underfunded, overlooked, and treated as a minor league by institutional capital. What changed in Q4 suggests the country might finally be getting taken seriously—at least by the subset of investors with real conviction.

Look at who showed up for Micruity’s $20m Series A. Rebalance Capital and Nationwide Ventures co-led, but the roster includes J.P. Morgan Asset Management, State Street, TIAA Ventures, and the Reinsurance Group of America. These aren’t scrappy angels. These are institutional heavyweights backing a data infrastructure play in retirement income. That’s institutional-grade validation for a Canadian startup in a boring-sounding category.

Micruity targets something real: the broken plumbing of American retirement. 401(k) plans serving 100+ million Americans were built for accumulation, not distribution. That’s a structural inefficiency, and fixing it is worth serious money. The fact that heavyweight investors see it that way says something about how FinTech funding matured in 2025.

It also says that Canada’s FinTech ecosystem isn’t just surviving the consolidation wave—it’s becoming a magnet for infrastructure plays that solve actual problems. That’s a shift from the 2019-2021 era when Canadian venture money chased consumer apps and payment gimmicks.

The Warning Hidden in the Data

Before you break out the champagne, consider this: concentration isn’t always healthy. Eighteen deals generating $1.6 billion is strong, but it also means capital is clustering around proven teams and obvious problems. Seed-stage activity probably collapsed. Early-stage founders in Canada are likely having a harder time than ever raising their first institutional round.

The Q3-to-Q4 comparison is actually telling a story about deal velocity and timing, not just market strength. Yes, Q4 smoked Q3, but that’s partly because 2025 was volatile overall. FinTech funding globally has been choppy—not recovering to 2021 levels, but no longer in free fall. Canada appears to have captured some of that rebound, but on a smaller base.

Here’s the thing: a 52% year-over-year jump looks juicy in a press release. But you’re comparing Q4 2024 (which was itself weak) to Q4 2025. The real test is whether Q1 and Q2 2026 sustain this momentum or whether Q4 was a seasonal anomaly—year-end capital deployment before tax year-end.

What Actually Happened

There are a few plausible explanations for why Q4 2025 broke through:

First, interest rates finally stabilized. The Fed held in November and December, removing the uncertainty tax that haunted venture capital in 2024. That breathing room alone can unlock large institutional commitments.

Second, the FinTech sector matured. The companies left standing—the ones raising Series A and B rounds—are the ones with unit economics, customer traction, and defensible technology. That’s exactly what Micruity represents: a play on infrastructure, not a consumer app praying for network effects.

Third, cross-border institutional capital is flowing into Canada again. That J.P. Morgan, State Street, and TIAA participation in a Canadian round suggests the U.S. money is comfortable with Canadian FinTechs as LPs increasingly demand geographic diversification in their venture allocations.

It’s not a euphoria-driven rally. It’s pragmatic capital doing pragmatic things.

The Bottom Line

Canadian FinTech funding rose 52% year-over-year in Q4 2025, but the more important metric is that the average check size jumped nearly 10x compared to Q3. That signals institutional confidence in a narrower set of companies solving real, structural problems. Micruity’s win—and the heavyweight syndicate behind it—suggests that Canada’s FinTech moment is finally arriving, but only for the companies worth real institutional capital.

The question now is whether this is a sustainable shift or a Q4 blip. Early 2026 data will tell. But if you’re a Canadian FinTech with product-market fit and a differentiated solution to an obvious problem, the funding environment just got meaningfully better.

🧬 Related Insights

- Read more: PayPal, Convera, and Nium Are Betting Big on Stablecoins—But Regulators Aren’t Done Writing the Rules

- Read more: SoFi’s Big Business Banking Bet: Can One Platform Really Handle Fiat and Crypto?

Frequently Asked Questions

What was Canadian FinTech funding in Q4 2025? Canadian FinTech raised $1.6 billion across 18 deals in Q4 2025, up 52% year-over-year from $1.1 billion in Q4 2024.

Why did average deal size jump so much in Q4 2025? Average deal value reached $89.1m per transaction in Q4 2025, up 34% from $58.6m in Q4 2024. This reflects investor concentration on larger, higher-conviction bets in companies with proven traction, rather than increased deal volume.

Is Canadian FinTech funding sustainable going forward? That depends on Q1-Q2 2026 data. The Q4 surge partly reflects year-end capital deployment and stabilized interest rates. Early 2026 will reveal whether this represents a structural shift in investor confidence or a seasonal anomaly.